Indicators point out that the loss of momentum in the manufacturing sectors followed a downward trend parallel to the extreme depreciation of the TL and rising inflation following the interest rate cuts that started in September 2021. In the loss of momentum, there is an acceleration in the third quarter. On the other hand, as mentioned in this column last week, despite the suppressed interest rates reaching record negative levels, the downward trend in commercial loans also gives important clues about the nature of the contraction in production. The table that the data points to is as follows:

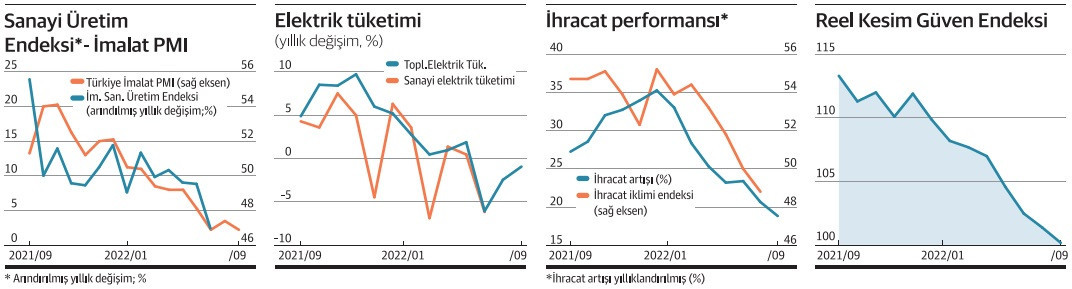

Industrial production: The Industrial Production Index had reached its peak level in December 2021, with the recovery after the pandemic wore off. The index came down 13.7 percent in July compared to the same period. The index, which has fallen by 4.7 percent in the last three months, is 2.4 percent higher than last year’s level as of July. Contraction is predominantly mining and energy welding. Other indicators regarding production point out that the contraction has accelerated since August.

Electricity consumption: Almost 45 percent of the total electricity consumption is the consumption of the industry. The last of the data, which was announced with a delay of three months, belongs to July. It is noteworthy that the electricity consumption in the industry decreased by 6.1 in July compared to the previous year. The decrease in total electricity consumption, which can be monitored in the current way, in August and September implies that there was a contraction in the electricity consumption of the industry in this period.

Manufacturing PMI: Turkey Manufacturing PMI, which is considered a strong leading indicator of industrial production and growth, has been following a downward trend since December 2021, excluding the limited increase in August. The PMI, which fell below the 50 threshold value in February, dropped to 46.9 in September, and the number of consecutive periods in which the index was below the threshold moved to the seventh month. While the slowdown in production left 10 months behind, the increase in inventories reached its fifth month as new orders weakened, and was measured at the fastest pace since February 2012.

Export: The annual rate of increase, which had risen to the range of 30-35 percent since the last quarter of last year, fell below 20 percent in September. Part of the increase was due to prices driven by higher input costs. Export Climate Index has been following a downward trend since March. The index fell below the 50 threshold value in August for the first time since 2013, excluding pandemic closure periods. The stagnation in foreign markets is expected to further reduce the increase in exports.

Confidence index: The direction of the Real Sector Confidence Index, which monitors the sector’s activity indicators such as orders, production, stocks and employment, and seasonal expectations regarding the economic outlook, has been following a downward trend since September 2021. The decline has continued uninterruptedly since April. Firms foresee a contraction in employment for the first time in 28 months, as well as production and orders in the next three months.

Experimental interest The bill of his policy is growing…