What is the difference between the 2001 crisis days and today? They asked me about this recently. If you ask me, for the broad masses of the people today is worse than it was then. Why? In 2001, we had a more partial problem with banks and companies, it directly affected fewer of our citizens, and in fact, the problem was more manageable. Not so today.

Today, our companies and banks are doing well. However, the rapidly rising inflation and the increasing cost of living caught all segments of the society unprepared and affected them badly. However, in 2001, we were considered to be bad for inflation. All segments of society, from the bottom 20 percent to the top, are aware of the rising prices today. In fact, everyone follows the price of the item they use the most according to their consumption pattern. Some the price of coffee at Starbucks, some the price of bread.

“Do you realize how much a hamburger costs a coke?”

In this framework, everyone is trying to increase their income in their own way. Bizim Sarp recently answered the question of pocket money, “Do you realize how much a hamburger and a coke cost now?” he opened it. He’s right too. Where is the problem? In fact, prices have never been in the process of rising so fast in the periods I remember. And we’ve never been so caught off guard.

Previously, yes, we lived with high inflation for many years, but back then there was an indexing mechanism to align income flows with rising prices. It is true that we owe the inertia of inflation to that mechanism, but there was a ready-made morphine mechanism that was automatically activated to make us feel the pain of high inflation less. Not now.

When we look at it today, it seems bad, but at the same time, the fact that we have come to this day in a short time and we are not used to pain now is also a chance in terms of fighting inflation. The fight against inflation lobby has a chance this time and if you ask me, it is possible to get results quickly.

The way to get quick results is the Central Bank’s foreign currency Of course, he should stop gossiping about fields and focus on his own business. What is your own business? Of course, keeping the year-end inflation expectations under control. This is exactly what the Chairman of the US Federal Reserve said recently, “We will not let inflation expectations get out of control”. The main job of the Central Bank.

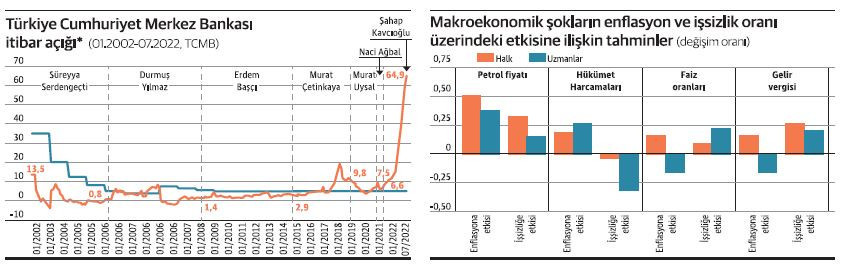

Inflation expectations broke in 2022

The difference between the year-end inflation expectations and the inflation target is called the reputation deficit of the central bank. We have been following the reputational gap since we switched to inflation targeting. If there is no target, it is necessary to look at other parameters to measure the reputation of the bank. The chart below shows the credibility of central bank governors since 2001 when we switched to inflation targeting.

What are we seeing? The reputation deficit of the Central Bank was 6.6 points at the end of 2021, when Naci Ağbal was dismissed. He was only so far off target. Now it’s 64.9 points in just one year. Why? There are no targets left, the waits that have broken their rope and gone. However, the goal essentially exists to keep the expectations under control.

Since the day we started inflation targeting, there has never been such a big explosion, never such a rapid loss of reputation. Let’s first identify a situation. Look, at the point we started targeting, the period of President Serdengeçti, who managed the process? Is there such a figure even when we are just starting this business, at the very beginning of the credibility building process? No. There are now.

What is this? Is it possible to find a better indicator that the bank neglects its main job, to keep inflation expectations under control? Not. This is what’s going to be fixed. The bank’s return to its original business as soon as possible. What is the reason for the cost of living today? This is inflation expectations that have gone out of control. It is because the Central Bank has forgotten its main job. Dot.

The determination of “interest is the reason, inflation is the result” does not belong only to Tayyip Bey, let me also express it.

So, how are inflation expectations shaped? There, a recent study revealed that technicians and the public do not think alike about the inflation dynamics of people on the street. Central banks ask a series of market professionals working at banks and universities about their year-end inflation expectations. The reputation gap above reveals what market professionals think about the management of our central bank. Disreputable. So what do people think? We do not know him in Turkey.

The results of the study, which was conducted in the USA with 6500 subjects and recently published in Review of Economic Studies, a prestigious journal in its field, are shown in the second chart. Here, we see that market professionals and the public do not have a similar view on inflation and unemployment dynamics. Two things stand out in particular. First, while market professionals say that raising the Central Bank’s policy rate will reduce inflation, the public believes that raising the policy rate will increase inflation. Second, while market professionals think that raising taxes will help contain inflation, the common man believes this move will raise prices. One of the parties speaks on the basis of its technical knowledge, while the other acts on the basis of their experiences in life or hearsay.

It is clear that while the people on the street consider the impact of the measure on firms and their pricing behavior and costs, market professionals look at the impact of the measure on household demand and spending patterns. Why? The transmission channels are different. One is supply side and the other is demand. So what comes out of here? In this new age, it is necessary to rethink central bank communication policy more comprehensively.

When we say to control the inflation expectations, since it is important to affect the spending pattern and pricing behavior of the people on the street,interest It is necessary to design a healthy communication policy that also aims to correct the wrong assumption of “reason, inflation, result”.

The Central Bank needs to design its communication policy for the control of inflation expectations, not only by appealing to the technical knowledge of market professionals, but also by taking into account the urban legends that households believe. This is the result of the study. In this new age where the individual is empowered, it is necessary to think more comprehensively about communication policy. The Turkish experience is a good example of why the issue should be handled more comprehensively. After all, the politician is not a market professional, but one of the people in the street. But I guess it’s clear. Why are we here today? Of course, because our central bank is not doing its main job. The bank must first realize that the communication policy does not mean “don’t take those expensive loans, bro” and determine a healthy communication policy that takes into account the superstitions of both market professionals and the man on the street.

In this case, let me remind you of the “Catalogue of the Superstitions of the End Times”

I started the “Catalogue of the Superstitions of the End Times” in the pre-apocalypse of 2001, in the dark age of Turkey’s economy. Finally, all hell broke loose. Honestly, I was extremely hopeful that I wouldn’t have to open that notebook again. But that did not happen, since 2018, the dark age of the Turkish economy has started again.

When Turkey forgot what it was trying to do and started to falter, as usual, at first it was confused. When the target or the credibility of the target was lost, a voice began to emerge from every head. The superstitions came to the fore. Those who want can also say “Urban Legends Notebook”. Recording urban legends of economics is, at the very least, fun. People are less angry.

Why now? Because we have now seen that the proposition “interest cause, inflation result”, expressed by the most authoritative mouths, actually means “low interest cause, high inflation result”. In fact, Moody’s downgraded Turkey’s rating to B3 last week and underlined the issue of “low interest is the reason, high current account deficit is the result”. Considering that after B3 is now a deluge, it’s time to get back to the catalog business.

What was Turkey like before 2001? a snapshot

Everyone remembers an inflation adventure for himself. The price of coffee for some, the price of gasoline for others. In fact, I have always followed what inflation is like through book prices. I would like to remind those who do not know about Turkey before 2001. In my childhood, in the late 1960s and early 1970s, the prices of books were printed directly on the book. Then, with the inflation period that started at the end of the 1970s, the price of the book began to be written on a self-adhesive label over that printed price. Such was the 1980s. Also in the 1990s. The price of the book changed as it stood on the shelf. The situation was not as bad as the German inflation of the 1930s. We didn’t have to carry around a sack of Turkish Lira or something like that. The clippings were constantly growing.

The numbers on banknotes such as 500 lira and 1000 lira, which will be released soon, were growing. At that time, the staff of the bookstores would calmly change the labels of the books while you were looking at the books. Then gradually, publishers stopped printing the price of the book directly on the back of the books. It was always changing anyway. The price was now written on the price tag. There was no longer a printed price underneath the self-adhesive label. That price was already changing in a week. Turkey’s adventure of high inflation came to an end approximately in 2004.

Inflation has returned to single digits for the first time in nearly three decades. At that time, I was on the Central Bank Monetary Policy Committee. When I was appointed there in 2001, inflation was around 80 percent. It fell to 8 percent in 2004. Either the program was good, or there was China, which produces cheap goods in the world. Anyway, the important thing is this: Inflation ceased to be a problem for Turkey at the beginning of the twenty-first century, and this is how we made the next leap forward in the industry. That’s newer. Twenty years ago.

Inflation ceased to be a problem for Turkey, but Turkey began to lose its inflationary memory only in 2011. The process of printing book prices directly on the back of the books, which first started sporadically and then accelerated, reappeared that year as evidence that the inflationary memory began to fade. Only eleven years ago. Now I guess we’ll be back to the beginning soon. It’s not good, but it is. Add to this the restructuring of value chains and the diminishing effect of China’s cheapening of prices. This is not a good sign. It will consume us again. See how the old period was, let me leave a photo here. I bought “The Song of Dodo” by David Quammen, in which he describes biodiversity, in the early 2000s. I recently found it again in my library.

There are two aspects in the photo: First of all, the foreign book has a price in lira on the label, as the exchange rate stability is relatively ensured. Otherwise it wouldn’t have. The second is the price of the book: 7 million 490 thousand liras. If you look at prices and salaries these days and say “No more”, let me remind you that we could pay 7.5 million liras for a book, our salaries were billions of billions at that time. Please don’t happen again. See, last regret doesn’t help. Fortunately, the prospect of a solution is not far off.